For me, when the Forbes MLB valuations are published every March, it’s like Christmas nine months early. Forbes goes to the trouble of sleuthing around baseball even as team financials are meant to be heavily safeguarded. It provides this blog and others with that last bit of off-the-field news just before the season starts in earnest. Thanks to Mike Ozanian and Kurt Badenhausen for putting the 2013 edition and previous editions together (full list).

2013 Forbes franchise valuations with some additional extrapolation

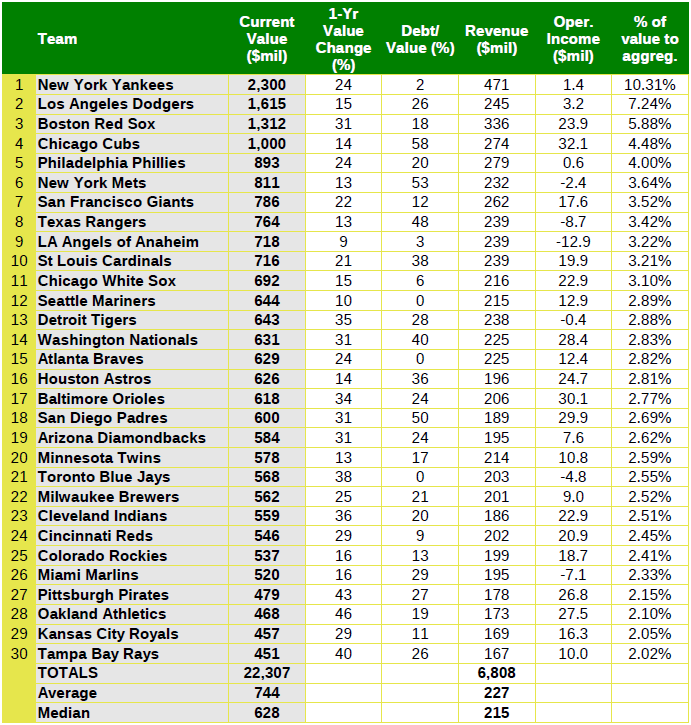

As expected, the combination of the Dodgers ($2.1 billion) and Padres ($600 million) sales plus new TV contracts on the horizon pushed franchise values up. Way up. No team has a valuation lower than $450 million. Credit also goes to MLB Advanced Media, whose expanding product line includes MLB.tv, the At Bat apps for phones and tablets, and Tickets.com. Forbes estimates that if it were public, MLB AM could be worth $6 billion on its own. Slow, deliberate baseball is not the kind of enterprise one thinks of when looking for examples of startup culture, yet the success of MLB AM is undeniable and felt in every owner’s pocketbook every year.

These new valuations result in an aggregate $3.5 billion rise over last year. The A’s, who were last in 2012 with a $321 million valuation, are now 28th with a $468 million valuation. That’s a whopping 45.8% gain, all without negotiating any lucrative new media deals or the benefit of new ballpark revenues. $468 million is reflective of the new national TV deals that MLB will receive starting with the 2014 season. Even with the increase, the A’s are $160 million below the media franchise value and $276 million below the average valuation. For reference, the big market Giants got a $143 million boost and moved from 9th to 7th place. As we observed last year, the bubble is real. Thanks to baseball’s solid, diverse revenues, the bubble is also not going to burst anytime soon.

Debt that the A’s are carrying appears to be unchanged at around $90 million. This is no surprise because haven’t signed any big contracts since Yoenis Cespedes. By staying put, the debt-to-value ratio has gone down from 28% to 19%. That’s important because if Lew Wolff is going to build a new stadium in the next several years, it’s best to keep debt relatively low and operating income high so that they can borrow big for a ballpark. The downside of that conservative approach is that much of the A’s young talent could be out the door sooner rather than later, as we’ve seen frequently over the years.

Forbes also explained a little of their methodology this go-around.

Our team valuations are enterprise values (equity plus debt) and are calculated using multiples of revenue. Thus while teams value MLBAM and BELP on their balance sheets on a “cost basis,” which understates their true value, we incorporate market value estimates for those assets. Two more significant ways our accounting differs from the P&L statements of many teams: we include revenue teams keep from concerts, soccer games and other events at their ballparks; and we deduct from revenue stadium debt payments that are paid with stadium revenue. In short, our team values are meant to reflect what a buyer would be willing to pay in an arms-length transaction and our operating income measures are meant to indicate how much cash is generated.

Basically, Forbes is making the distinction that their numbers are reflective of how each team is run as a business, as opposed to P&Ls reported to baseball which may be products of arrangements designed to hide or minimize secondary revenue sources and expenses. While commissioner Bud Selig and the owners will downplay or write off Forbes’ figures, we can feel a little more confident in their soundness based on what they’ve dug up and the new industry information that has come in over the last two years.

Wait, what’s that BELP thing? BELP stands for Baseball Endowment Limited Partners, a sort of internal baseball hedge fund. It was started when the owners collected the franchise fee for the Washington Nationals into another partnership called Baseball Expos Limited Partners. The owners and Selig decided to reinvest that $500 million instead of distributing it to each ownership group. The strategy has literally paid dividends for the owners, because once money from BELP I was rolled over into BELP II, baseball started getting major profits from the fund. BELP was first exposed a few years ago when Deadspin received leaked financials from several teams, but the kinds of investments BELP chose to venture into were kept under wraps. In the past, I’ve put BELP in the category of “Other” when accounting for Central Revenue. I’ll probably break it out going forward, though that will be based entirely on estimates since BELP isn’t public.

The main article ends with a few notes on the A’s, which is somewhat unusual. It’s pointed out that the A’s got another fat revenue sharing check of over $30 million, and an attendance boost coinciding with the team’s division crown. Local revenues continue to lag, so revenue sharing and central revenues are (more than) keeping the team afloat. That’s a double-edged sword, as it gives critics of Wolff and John Fisher ammo to say the team is again being “cheap” with regards to how it runs the team. Now that payroll is taking up less than 40% of revenues, it’s worth asking if the team is saving money – perhaps for a ballpark. If the marginal cost per win in terms of talent is difficult to justify (see: $11 million/year for Kyle Lohse), filling the piggy bank for a ballpark wouldn’t be a bad way to go.

Of course, there’s another side to the revenue-payroll debate. With all of the money that’s coming in, Wolff, Fisher, and the other partners would have to be absolutely nuts to sell the team. They’ll only get more money next year, which they can invest in one of their cornerstone players. The windfall also makes it even more difficult for interested East Bay parties such as Don Knauss to get the team. Last year, as the Dodgers and Padres sales happened, I predicted that the A’s value would hit at least $500 million. They haven’t that number yet, but they’re almost guaranteed to hit it in 2014. So again, that puts the cost to keep the A’s in Oakland at $1 billion: $500 million for the team + $500 million for the ballpark. Good luck with that.